We have all heard about the well known disasters such as Baby P, Deepwater Horizon, Staffordshire Hospital and the Fukushima Nuclear power plant explosion, examples of organisational systemic failure to deliver the intended results.

We have all heard about the well known disasters such as Baby P, Deepwater Horizon, Staffordshire Hospital and the Fukushima Nuclear power plant explosion, examples of organisational systemic failure to deliver the intended results.

In all these cases, the subsequent inquiries showed that the indicators or risk of failure existed before the disaster occurred. The same applies to other performance issues, be that a lost customer, not meeting sales targets or failure to meet any other business objective – by the time the poor performance shows up on a graph it has already happened, it is too late and it can’t be undone. Have you ever wondered why after something doesn’t work as it should, someone quite often says ‘I knew that would happen’? So what risk is your organisation running right now, risks that are often invisible to traditional audits until the unintended event outcome emerges and by that time the damage is done?

What is the point of only auditing what has already happened; its like trying to drive your car by only using the rear view mirror. Looking at ‘where you have been’, which is what most Certification Bodies do, provides little evidence of future capability – and it is future capability that either delivers future results and/or creates the risk of not doing so.

Assessing capability to manage future results

The High Performance assessment (HPA) is a UKAS accredited Certification Body that adopts a unique online approach as an integral part of its certification programme. We do this because it:

delivers an approach that transcends the constraint of the human auditor, raising above the current man-day model, creating and making available a deeper picture of organisational performance, conformance and risk

|

Scored risk profile of capability from which you can drive improvement:

Benchmark data by clause, by dept and by groups of people for greater improvement identification:

|

How does 21st century auditing work?

Auditing is a risk management tool. To manage the cost, collect and analyse the data needed The HPA uses an IT-based automated system that requires very little involvement from those being assessed. The Technical Report produced provides the evidence needed to reduce and focus the more intrusive human audit visit.

‘Wow – wasn’t expecting such comprehensive info from the online assessment. Already have some new (several startling) insights and host of ideas for change. I need to digest this and may come back for some better understanding as I get through this.’ – Laurence Goode, Director of Broughton Controls and Chairman of the PSSA

What is different about The HPA is not that we follow different rules to other Certification Bodies, just that over a number of years we have researched, developed and tested a different and proven approach that recognises and addresses many of the current problems associated with auditing.

Getting more from your investment in internal auditing

Internal auditing suffers from the same issues and whilst many internal auditors strive to provide information that helps to drive their business forward they are, like all of us, constrained by our own human ceiling of competence. A level that creates a limit to what we are capable of providing for our businesses. Recognising that we need the help of additional tools to break through to a new level of auditing is key to moving forward.

What gets reported?

Both for certification and internal auditing purposes audit reports expose the level of risk to the key drivers of delivery performance and business objectives. These are influenced by the myriad of human interactions that take place everyday as people go about their normal business and we use these to provide the evidence needed for the assessment. Typical reports and real-world case studies are available, but as an example the reporting elements listed below are real.

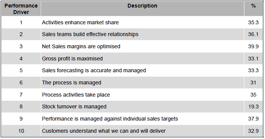

| Example 1 – Findings from an audit of a sales process.This involved people inside and outside the sales function as well as, in this case, customers. This created a much deeper understanding of capability, reporting risk to what the Sales Director is charged with delivering |

|

|

|

Example 2 –Findings from an audit of a manufacturing process.These audit findings were generated from firstly understanding what the Management Team wanted to achieve and then gathering data on people’s behaviour in delivering this. Analysis identifies the risks | |

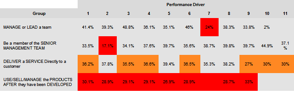

| Example 3 –Exposing performance riskBenchmark results between groups of people to expose where the real risk is emerging.In this case the impact of risk to performance is being felt by those who use or sell the products, but not necessarily by those who manage their development. |

|

|