One of the main objectives for the Business Management Standard BMS75k was to address the need to establish and verify Business Decisions with the same degree of control that we afford products and service quality.

One of the main objectives for the Business Management Standard BMS75k was to address the need to establish and verify Business Decisions with the same degree of control that we afford products and service quality.

In dealing with the individual clauses and subjects of the management standards, the subject of risk has to be considered as this is significant in ISO9001:2015: and even more so for the Business Management Standard BMS75k which commends the use of planning and preparation in respect of risk management and control.

In each quotation, design, contract, purchase or product run there is a risk in setting the quantity, price, program or setting the quality boundary and such risk is a business decision which should be checked, tested, justified and verified as correct before implementing.

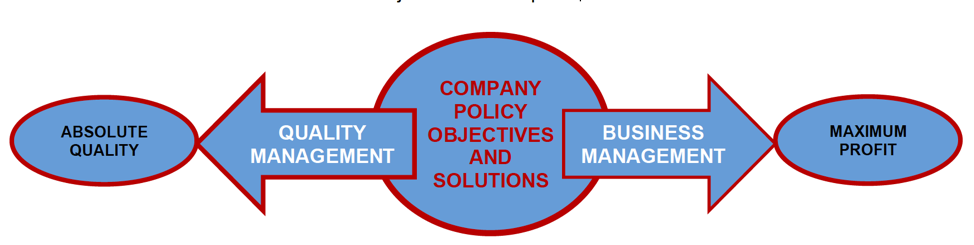

The principle difference in the standards is that quality systems see risk as detrimental to product and service quality, whereas business recognizes the need to embrace risk as an opportunity. Indeed it has long been the view from economists that risk is the moral justification for profit.

Now we all know that good quality leads to good profits with less waist and greater customer satisfaction however, “Quality at Any Cost” or “Absolute Quality” is irresponsible as a commercial solution for Business.

THE QUALITY OF MANAGEMENT

The management of quality is well established and has the mitigation for risk in product and service release challenged effectively with established quality control methods and practices. But the quality of management is not the same as the management of quality and the main challenge for the Business Management Standard BMS75000:2020 was to provide an equal control and defence for the business decisions made as part of a management business program,

Risk is found in the text of the following clause subjects of ISO9001:2015,

- Clause 0.1 General

- Clause 0.3 Process Approach

- Clause 0.3.3 Risk Based Thinking

- Clause 0.4 Relationship with other management systems

- Clause 5.1.1d Leadership

- Clause 6.1.2 Planning

- Clause A4 Risk Based Thinking

- Clause A8 Control of externally provided process, products and services

At no stage in the application of these clauses does the Quality Standard advocate seeking to engage risk and presents risk as nothing more than something to avoid or mitigate against.

We have all seen our favoured and highly prized suppliers fail because we just could not afford the cost of the quality they were insisting on producing, or we were insistent on having something aspiring to absolute quality.

Many of us in the quality profession at some stage in our employment faced redundancy as a result of our employers maintaining similar policies on absolute quality. When the requirement for absolute quality is such that it prohibits the products sale at an acceptable price, or takes too long to produce, the market will look elsewhere, and find that which is acceptable. So we should seek to provide and maintain the “Right Quality” for the product and service in question.

The concept of Quality Defence is offered in this respect as a solution and has 5 main contributors from which a defence of the Right Quality can be presented. In defence of quality we must seek to determine and defend “What it is and What it does” which is proven beyond reasonable doubt by adopting the following methodology:

Quality Control

Planning and application of stage and final measurements to confirm and ensure conformance to specified requirements or to segregate that which is non-conforming.

Quality Compliance

Verification by acceptable means of the correct specified process, product, service or occasions’ quality attributes and advantages.

Quality Assurance

The methodology and program for the systematic monitoring and evaluation of the various aspects of a project, service, or facility to ensure that standards of quality are being met.

Quality Improvement

Management and control of actions taken within an organization to increase effectiveness and provide added benefits to the organization, stakeholders, customers and other known interested parties.

Quality Management

Management and influence of all quality related processes and factors that can improve or put at risk the realization of an agreed or desired quality of products and service.

The above definitions are selected, modified and developed not only to assist in the concept of Quality Defense but also to incorporate a number of dictionary and authorities’ own definitions as well as avoiding infringement of copyrights.

QUALITY CONTROL

The old saying “Prevention is Better than Cure” sits well when it comes to defending quality, because quality control is directed at preventing the inadvertent release of non-conforming products or the delivery of sub-standard services,

So the very first line of defence is Quality Control, consisting principally of planning and application of stage and final measurements to confirm and ensure conformance to specified requirements or to segregate that which is non-conforming.

ISO9001:2015 Risk Based thinking concludes an effective quality control regime is needed, implemented, maintained and effectively managed, and the quality produced is well defended and secure within the boundaries of the organisation. In addition, the integrity of the product and service is assured and the products or service provenance provides the confidence for the release of the work done.

The task for the new Business Management Standard was to find and proscribe the same degree of verification for Business Decisions which we enjoy by applying Quality Controls to products and service delivery.

QUALITY VERIFICATION

New work being done at Q-Share International on a Quality Verification Standard BMS77000 being prepared for publication in October 2020, is relying on some well established but forgotten techniques in grading the degrees of quality we can apply to our quality controls. This is demonstrated by way of undisputable records for each verification occasion that can be challenged, and be traceable to a recorded position in time and event.

The Quality of Compliance has predominantly five degrees of assurance, originating with the DIN Standard 50049 later referred to in EN10204 for product certification and documentation.

1st Level Self Certified Declaration of Compliance

Here the manufacturer confirms compliance with a customer’s order as a basis for release.

Provence is a statement of compliance with the order by the manufacturer without test results.

2nd Level Process Verification Confirmation

Here a declaration of compliance with the order by the manufacturer is give as a basis for release based on non-specific process verification inspections (tests) by the manufacturer.

Provence is a statement of process deployment on a given order by the manufacturer without test results.

3rd Level Batch Specific Test and Inspection.

Here the results taken from a batch indicative of the product supplied derived from specific test results from a batch inspection and testing are provided as a basis for release.

Provenance is a batch test certificate issued by the manufacture traceable to the batch from which the product has been produced issued and signed by manufacturer’s representative, who must be independent of the manufacturing department such as the Inspection department or test house manager/supervisor.

4th Level Product Specific Test and Inspection,

Here the product supplied is traceable to test and inspection results specifically taken and recorded for the product being supplied as a basis for release.

Provenance is a certificate or inspection report produced by the manufacture with specific test and inspection results.

The certification would be identified with serial numbers or idents which can be also observed in some form on, or attached to, the product itself.

5th Level 3rd Party Attendance and Verification

Here the product supplied is traceable to test and inspection results specifically taken and recorded for the product being supplied and a recognized and qualified independent examination authority attends and witnesses the test and inspection activities to confirm their completion and correctness as a basis for release.

Provenance would be a certificate or inspection report produced by the manufacture with specific test and inspection results endorsed by the 3rd Party Inspection Authority.

The certification would be identified with serial numbers or idents which can be also observed in some form on or attached to the product itself together with the seal or insignia of the employed 3rd party organization and the signature and stamp of the attending witnessing inspection authority.

The intention when preparing the Business Management Standard BMS75k was to convert these practices to the verification of Business Decisions which we achieved as follows:

MAKE OR BUY

The first consideration a company will make when making a decision on seeking a solution to a problem will be to “Make or Buy”. Even the continuity of a current practice or process using existing capacity is invariably a commitment to make, as opposed to purchase or hire.

The mitigation or limiting of risk is a principle consideration in this decision which is handled as follows:

6.1.2 Make or Buy Analysis and Planning

The Company shall demonstrate that in all principle activities the costs and benefits of using internal acquired resources has been planned by comparing the options to purchase or hire from suitable suppliers or sub-contractors. Make or buy considerations shall include as appropriate

a) Associated risks and opportunities

b) Cost and value to the Company of each option

c) Timeliness and program

d) Totality of the problem solution and transfer of ownership

e) Relative goods, or service quality

f) Availability and sustainability of capacity

g) Loss of experience, know-how, goodwill and other intellectual property.

The make-or-buy decision shall be reviewed from the full perspective of available facilities and resources with due consideration to each option and its impact on:

h) Maximum utilization of facilities and resources;

i) Transfer or conversion of underemployed facilities and resources;

j) Maintenance, reduction and disposition of facilities and resources;

The impact on the Company’s stakeholders shall be considered and in particular, those persons or authorities that can affect, be affected by, or perceive themselves to be affected by the make or buy decision.

The practices for make or buy business activities shall be the subject of a documented practice. (See 5.4.2)

The decision to make or buy shall be recorded and the record recognized as a controlled business record. (See 7.5.3.2)

PROCESS PLANNING, MANAGEMENT AND CONTROL

Project management and Planning of the company processes is addressed under clause 6.1.3 and 6.1.4. Here we seek to direct the control of risks inherent in the process of the company by project managing them.

Here we are required to plan and manage the operations within the control of the Company in a structured and controlled manner to meet requirements at acceptable risk, within the resource and schedule constraints. In addition business solutions must be project managed to achieve an effective planned solution, as well as to contribute to the learning within projects and continually improve the Company’s management capability. A documented practice or an equivalent method is specified as a requirement.

The need for a continuous improvement management project is specified as is a Business Program, to incorporating planned processes for business effectiveness and efficiency incorporating innovation flexibility, and integration with the Company’s own goods, services and processes. Process effectiveness assessment reporting is often referred to as PEARs and the practices for process planning and control needs to be the subject of a documented practice or an equivalent method.

OUTSOURCING AND SUBCONTRACT PLANNING,

Controlling risks is commended by the use of planning. Continuing to develop the concepts of clause 6.1.2, the BMS75k standard makes provision for the planning of outsourcing and subcontracting under clause 6.1.5 which reads as follows:

6.1.5 Outsourcing and Subcontract Planning,

The Company shall consider outsourcing those tasks and activities for which it has the capability to perform but insufficient resources to complete its obligations in a timely or effective manner.

Outsourcing or sub-contracting shall only be undertaken following a make or buy evaluation and assessment (See 6.1.2) when it is in the interest of the Company to do so.

Outsourcing of processes cannot absolve the Company of the responsibility of conformity to all customers, statutory and regulatory requirements. Outsourcing and sub-contracting shall be controlled to ensure:

a) Known or foreseeable risks have been mitigated by the action taken

b) No residual risk remains with the Company for which control is not exercisable

c) Cost and value to the Company is known or calculable

d) Timeliness and program are achievable or predictable

e) Ownership of the problem is transferred

f) Quality considerations are not compromised

g) Strategic business objectives and responsibilities are protected

h) Safeguards are provided against loss of experience, intellectual property, know-how, goodwill and provenance.

The outsourced, subcontracted tasks or activities shall be conveyed to the contractors in written form to ensure progress and completion can be verified by each party involved in the agreement. Additional available controls shall be considered through the application of clause 8.4 were appropriate.

The practices for out-sourcing and control shall be the subject of a documented practice or an equivalent method. (See 5.4.2)

GOODS AND SERVICE PLANNING ANALYSIS AND REVIEWS

The final clause in section 6.1 of the Business Management Standard is given over to the subject of planning and analysis of the company products and services.

Here we are required to plan, review and analyse available data for the goods and services produced by considering and preparing for the following:

a) The introduction and withdrawal of goods or service

b) Risks associated with the goods or service

c) Goods or service ownership, configuration and responsibility

d) Goods and service costing, sales, revenue, profits, forecasting and development

e) Understanding of the customers’ needs and use relating to the goods or service

f) Goods and service development and improvement to exceed customers’ expectations

g) Suitability, integrity and traceability of programs, materials, components, processes and services used

h) Selection and partnering of suppliers and their contributions to the goods or service

i) Produceability, inspectability and criteria for correctness and completion of the goods and service

j) Ownership of goods or service intellectual property, patents and licenses

k) Goods and service reliability, availability and maintainability

l) Goods and service integrity, precautions against counterfeit goods and safety in use

m) Goods and service compliance with specified standards, known expectations and statutory instruments

n) Obligations in respect of migration, retirement, obsolescence and replacement

o) Recycling or final disposal of the goods and service at the end of its life.

p) Directions to and contributions from other internal operations and activities within the Company

These aspects and applications of the goods and services has to be assessed, analyzed and reviewed at planned intervals to improve the goods and service success during each of the phases of its life cycle (development -introduction – growth – maturity – decline).

As part of each assessment or review, the Company must demonstrate:

q) An understanding of how the goods or service works within its known applications,

r) The resources, including know-how, needed for the continued production or delivery of the goods or service

s) The resources and arrangements needed for the in –service support of the goods and services

t) Obligations and commitments for suitable arrangements to provide for replacement of obsolete items.

u) The legal and statutory requirements applicable to the production, sale and use.

v) Protection and provision for recourse against counterfeit goods and services.

The analysis and review of goods and service planning needs to be recorded as a controlled business record and the practices for goods and service planning analysis and reviews, shall be the subject of a documented practice or an equivalent method.

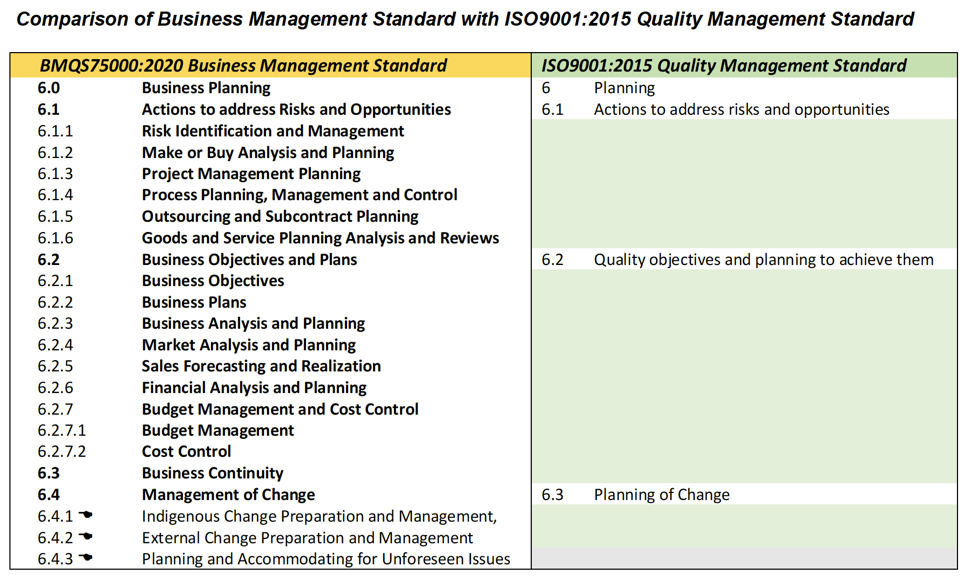

It is recognized that the subject of planning has been developed much further than the quality standard ISO9001:2015 has given over to the subject, but this is because Business Management is not the same as quality management and business decisions are less-tangible and far more speculative than a product and service requirement would demand.

This will be discussed in our next article which will tackle the question of Business Objectives and Plans.

Bio:

Godfrey Partridge

Q-Share International Limited CEO and President. Now stationed in the United Kingdom tasked with the administration and promotion of the Q-Share Group from an international prospective with operations now in the UK and USA directed at promoting improvements in Business Management through the use of Quality Assurance and the Quality of Compliance.

Contact information:

828 774 0763 (Work)

qshare.qa@gmail.com