The Coronavirus pandemic (COVID19) continues to spread throughout the world despite the best efforts of governments and the medical community. With no vaccine becoming available in the near term and perhaps even in the long term we are faced with growing uncertainty. It seems that ever since the emergence of COVID19 that conflicting advice, information and guidance has exacerbated the situation and created a lack of trust on the part of the public on what measures to take. Wear a mask.

The Coronavirus pandemic (COVID19) continues to spread throughout the world despite the best efforts of governments and the medical community. With no vaccine becoming available in the near term and perhaps even in the long term we are faced with growing uncertainty. It seems that ever since the emergence of COVID19 that conflicting advice, information and guidance has exacerbated the situation and created a lack of trust on the part of the public on what measures to take. Wear a mask.

Don’t wear a mask. Social distance. Don’t social distance. The only advice that seems trustworthy is “Wash your hands”; and, that is something that we should do regardless of the pandemic – it’s good common sense.

This gets one to thinking though. Thinking about risk, tipping points, connectivity, touchpoints, consequences, etc. Are we at a tipping point? Will a long-term pandemic stress the world’s systems of healthcare, commerce, trade, supply, etc. to a breaking point? Will trade negotiations grind to a halt as fingers are pointed and claims are made about the origin of the coronavirus, unfair trade practices, human rights, geopolitical tensions, sovereign debt, stimulus packages, disenfranchised populations, climate change, pollution, etc. Will a confluence of events trigger a greater catastrophe? We see in the news that another pandemic strain – H1N1-G has the potential to become a pandemic. China reported possible cases of Bubonic plague recently.

While so much attention is being focused on COVID19 will we miss seeing a tipping point that creates the next great shock that ripples throughout the world? Could that tipping point actually be a positive rather than a negative event?

Entanglement: Rethinking Risk

In the book, “Spooky Action at a Distance” (George Musser), Jenann Ismael posits on the idea that physical locality may not be the deepest level of reality.

“One of the strangest aspects of quantum physics is entanglement: If you observe a particle in one place, another particle — even one, light-years away — will instantly change its properties, as if the two are connected by a mysterious communication channel.”

The idea of quantum entanglement — the ability of separated objects to share a condition or state — was once dismissed by Albert Einstein as “spooky action at a distance.” Over the past few decades, however, physicists have demonstrated the reality of this kind of “spooky action” over ever greater distances:

“Maybe particles in an entanglement experiment or galaxies on the farthest reaches of known space act strangely because they’re really projections — or, in some other way, secondary creations — of objects existing in a very different realm. ‘In the kaleidoscope case, we know what we have to do: we have to see the whole system; we have to see how the image space is created,’ Ismael says. ‘How do we construct an analogue of that for quantum effects? That means seeing space as we know it — everyday space in which we view measurement events located at different parts of space — as an emergent structure. Maybe when we’re looking at two parts, we’re seeing the same event. We’re interacting with the same bit of reality from different parts of space.’

About now, I am sure that you are beginning to question my focus on this article and perhaps my sanity. However, bear with me as I will tie “entanglement” to how we are approaching risk identification, management and risk appetite. Entanglement also relates to tipping points, touchpoints, complexity and a myriad of other potentially catastrophic situations cited above.

Let us rework the quotation and apply it to risk, uncertainty, risk management, etc. It might read thusly:

“One of the strangest aspects of risk management is entanglement: If you identify (observe) a risk in one place, someone — even one, light-years away – may also have identified the same risk and will take action to mitigate the risk. This will instantly change the risk’s properties for you, creating a need to consider your risk mitigation actions. This works both ways, depending on who acted first. And we do not even have to be in communication with each other. Risk is not static. Risk changes by each action taken to mitigate or leverage it. Much the same as the particle example used in entanglement – as if the two are connected by a mysterious communication channel.”

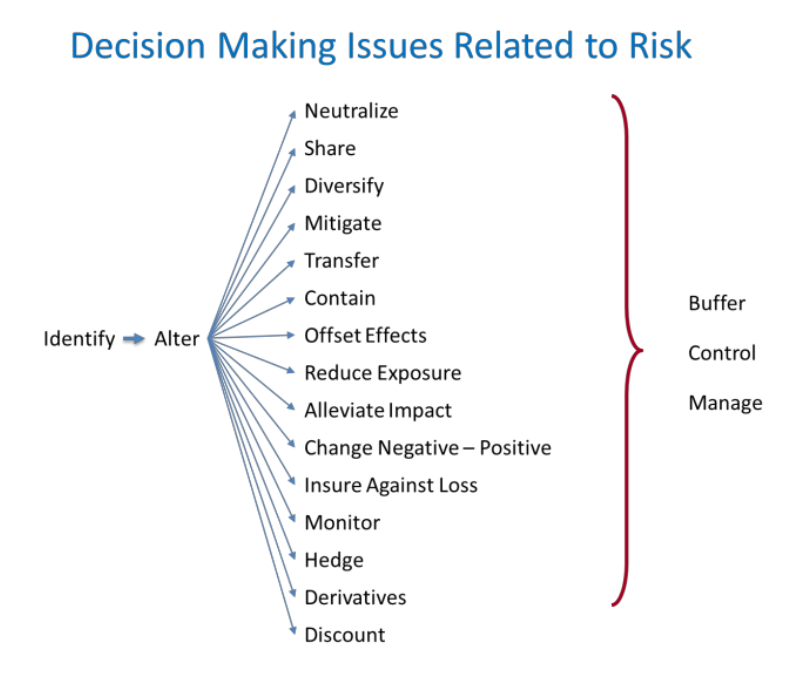

Now, multiply “entanglement” by all the identifiers of that risk and all the actions taken to mitigate this ever-changing risk (due to action changing the nature of the risk) and you get a potentially chaotic cascade effect. How is it that the world remains relatively stable when so much risk is constantly mutating due to mitigation? It’s relatively simple, our risk management activities are short lived and generally have been limited to certain types of risk management response, as depicted below “Decision Making Issues Related to Risk”.

So, after identifying and seeking to alter the risk through application of one or more of the mitigation options the assumed result is a feeling of buffering (protecting against), controlling and managing the risk. What does not get accounted for is the actions that others take that alter the risk, the actions that you have taken that alter the risk and the non-static nature of risk.

Before real problems can be solved, they must first be characterized in terms recognizable to all stakeholders. Unless one practices critical thinking, one is very likely to commit a very important error: Solving the wrong problem precisely. Critical thinking is the ability to see problems from multiple perspectives, expose critical underlying assumptions, challenge and reverse one’s assumptions and reformulate basic arguments.

Understand where we create the most value – now assess the risks and potential business impacts to a disruption of the ability to create value; build plans that are flexible and adaptable to the situation and the resources available, constantly monitor and assess risks (think like a commodities trader) to create Risk Parity.

Risk Parity is a balancing of resources to a risk. You identify a risk and then balance the resources you allocate to buffer against the risk being realized (that is occurring). This is done for all risks that you identify and is a constant process of allocation of resources to buffer the risk based on the expectation of risk occurring and the velocity, impact and ability to sustain resilience against the risk realization. You would apply this and then constantly assess to determine what resources need to be shifted to address the risk. This can be a short term or long-term effort. The main point is that achieving risk parity is a balancing of resources based on assessment of risk realization.

Risk Parity is not static as risk is not static. When I say risk is not static, I mean that when you identify a risk and take action to mitigate that risk, the risk changes with regard to your action. The risk may increase or decrease, but it changes due to the action taken. You essentially create a new form of risk that you have to assess with regard to your action to mitigate the original risk. This can become quite complex as others also will be altering the state of the risk by taking actions to buffer the risk. The network that your organization operates in reacts to actions taken to address risk (i.e., “Value Chain” – Customers, Suppliers, etc.) all are reacting and this results in a non-static risk.

The World Economic Forum (WEF) produces a Global Risk report annually. As depicted in their figure II, “The Global Risk Landscape 2020” “infectious Diseases” listed as one of its global risks this year, pandemic did not make it on the list as it had in previous years. I guess that the risk must have been assessed as too low to put it on the chart. You may argue that infectious diseases cover the pandemic risk category, but are you really comfortable with that argument? So, how did the experts miss the COVID19 pandemic risk? Was their attention focused elsewhere to the point of distraction? It seems that Climate Action Failure, Extreme Weather, Biodiversity Loss, Water Crises, Natural Disasters, Cyberattacks, Information Infrastructure Breakdown, Human-made Environmental Disasters were all perceived to be greater risks for 2020 with greater likelihood of occurrence and greater impact. Yet, the COVID19 pandemic (declared by the World Health Organization – WHO on 11 March 2020) seems to have superseded the eight (8) risks ranked higher than Infectious Diseases. Remember, a global pandemic was not considered a risk when the report was published. I wonder what the 2021 Global Risks Report will list? Let’s face it, we often get blindsided by risks that have been discounted, ignored or that we have not thought of with any great deal of effort expended to do an assessment of their potential. Predicting the future is never easy.

The World Economic Forum (WEF) produces a Global Risk report annually. As depicted in their figure II, “The Global Risk Landscape 2020” “infectious Diseases” listed as one of its global risks this year, pandemic did not make it on the list as it had in previous years. I guess that the risk must have been assessed as too low to put it on the chart. You may argue that infectious diseases cover the pandemic risk category, but are you really comfortable with that argument? So, how did the experts miss the COVID19 pandemic risk? Was their attention focused elsewhere to the point of distraction? It seems that Climate Action Failure, Extreme Weather, Biodiversity Loss, Water Crises, Natural Disasters, Cyberattacks, Information Infrastructure Breakdown, Human-made Environmental Disasters were all perceived to be greater risks for 2020 with greater likelihood of occurrence and greater impact. Yet, the COVID19 pandemic (declared by the World Health Organization – WHO on 11 March 2020) seems to have superseded the eight (8) risks ranked higher than Infectious Diseases. Remember, a global pandemic was not considered a risk when the report was published. I wonder what the 2021 Global Risks Report will list? Let’s face it, we often get blindsided by risks that have been discounted, ignored or that we have not thought of with any great deal of effort expended to do an assessment of their potential. Predicting the future is never easy.

5 Potential Shocks

Given that predicting the future is never easy I have nonetheless decided to peer into my crystal ball and provide a brief discussion on five potential shocks that could emerge in the near future.

Shock # 1: COVID19 Economic Recovery An oscillating recovery with one step forward and maybe two steps backward for a while and then a gradual smoothing of the oscillations and a resetting to another operational model may be the reality. Somethings will change forever and somethings will cease to exist. However, the path forward has always been marked by extinction and renewal.

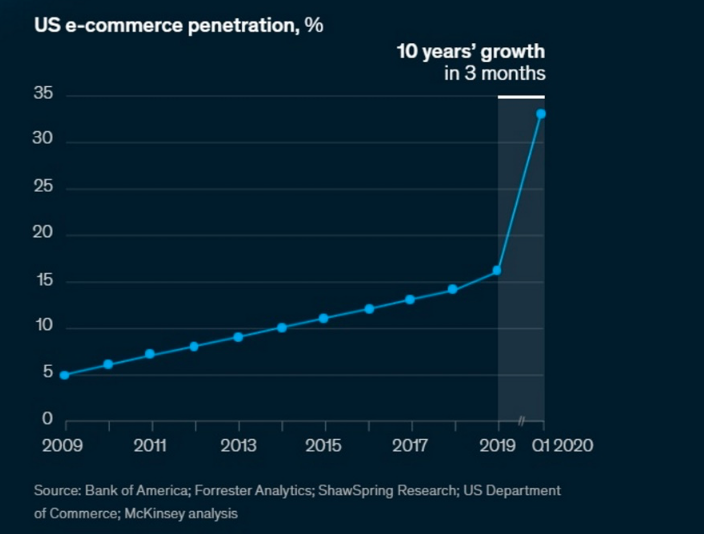

As depicted in the McKinsey illustration, US e-commerce has experienced 10 years’ growth in just three months as a result of actions taken to thwart the COVID19 pandemic.

As depicted in the McKinsey illustration, US e-commerce has experienced 10 years’ growth in just three months as a result of actions taken to thwart the COVID19 pandemic.

While this dramatic shift to e-commerce is impressive, the hospitality industry – restaurants, hotels and related services may not see a robust return to the pre-COVID19 days. The transportation industry is being devastated by the impacts to airlines operations worldwide. The cascade effect has seen oil prices drop to record lows and tenuously recover some of the pre-COVID19 price per barrel. Many who depend on jobs in the service industries could find that the road to recovery is one that will experience significant after-shocks.

And, let’s not be hasty; COVID19 is far from controlled, extinguished and no longer a threat. In fact, no one knows exactly when a vaccine will become available and how effective that vaccine will be.

Bottom Line: Economic recovery will not be rapid; many industries will shrink as a result of changing market preferences and a large segment of the population my never get out from under the yoke of debt.

Shock # 2: Geopolitical Tensions Explode into Armed Conflict Take your pick of potential hotspots that could explode – Russia – Ukraine, China – India, India – Pakistan, North Korea – South Korea, China – USA, Europe – Eastern Europe, Middle East – anywhere, Israel – Iran, Saudi Arabia – Iran, Iran – USA, the list could go on and on; but, I think you get the gist. Could we be on the path to a major global conflict? The tipping points are there and COVID19 has provided fuel for the fires. As I have written before, even a limited nuclear exchange between Pakistan and India involving small nuclear arms is projected to have major climate impacts that could see droughts, temperature drops and weather pattern changes lasting years. Of course, this could lead to an expansion of conflict as more and more nations are drawn into the situation.

Bottom Line: COVID19 has created the ideal storm for fanning the flames of global conflict. Instability, desperate measures to retain a status quo, loss of economic exchange due to trade policies; the smallest spark could set off a chain reaction that would be devastating.

Shock # 3: Sovereign Debt Triggers Global Depression Even while the markets continue to recover, the issue of Sovereign Debt hangs over us like the Sword of Damocles. It’s not just the US that is of concern, it is every major country in the world. Debt is rampant and governments are printing money as fast as they can. What will it take to lose confidence in a country’s fiat currency? Proponents of Modern Monetary Theory would argue otherwise. However, when people lose confidence and trust in the money of their country and governments start to lose trust in the exchange of debt structures (bonds, T-Bills, currency, etc.) we see that the financial foundation is wobbling as minor tremors portend potentially larger shockwaves.

Bottom Line: A COVID19 induced depression could lead to large scale conflict with significant consequences.

Shock # 4: A Great Reset Leaders of the world unite to declare a clearing of all debt from the books. Everyone starts over again with no debt obligations. While this may seem farfetched and in the realm of fantasy, it could happen. According to Wikipedia a debt holiday, debt relief or debt cancellation is the partial or total forgiveness of debt, or the slowing or stopping of debt growth, owed by individuals, corporations, or nations. From antiquity through the 19th century, it refers to domestic debts, in particular agricultural debts and freeing of debt slaves. In the late 20th century, it came to refer primarily to Third World debt, which started exploding with the Latin American debt crisis (Mexico 1982, etc.). In the early 21st century, it is of increased applicability to individuals in developed countries, due to credit bubbles and housing bubbles.

Bottom Line: A low probability, high impact event that would be rationalized by everyone afterward, expressing that they all saw it coming – a “Black Swan” by Nassim Taleb’s definition. According to a recent US Commerce report the US economy shrank at record 32.9% pace in second quarter 2020. While the statistics are interesting, as long as there is trust in the US Dollar as the reserve currency for the world these impacts can be absorbed. However, once trust is gone, we may have a problem in addressing the imbalances that are present. Just take a look at where the downturn is occurring – service industries, hospitality, gaming, restaurants, etc. Is the industrial base – heavy manufacturing, energy, being affected? Of course, by the cascade effect that links the service industries to the other sectors. We get fingers of instability that extend out from one touchpoint to another creating smaller shocks that cumulatively can produce larger shocks in another sector. These shocks reverberate creating tremors in adjacent touchpoint sectors. Suddenly you have a very wobbly global economy that is ripe for large downturns, economic chaos and geopolitical tensions that could lead to conflict. Could a debt reset alleviate the social ills that COVID19 has brought to the surface?

Shock # 5: The Internet Lynch Pin Collapses Any number of causes for a collapse of the Internet have been posited; from solar flares to hackers. While it seems impossible for the Internet to collapse, the reality is that the Internet is fragile in so many ways. As a touchpoint the Internet is immersion. One can think of very few areas that the Internet has not penetrated. However, there are fingers of instability that emanate from the Internet to almost every aspect of society. Connected as we are, could we survive a significant or total degradation of the Internet? How dependent is the world on this fragile underpinning? It goes beyond social media into the heart of all of the world’s critical infrastructures, geopolitical interfaces, financial, manufacturing, food producing, transportation, healthcare, etc. All one has to do is read the book, “One second after” by William Forstchen to grasp what a loss of connectivity would do to our technology dependent world.

Bottom Line: A low probability, high impact event that would be rationalized by everyone afterward, expressing that they all saw it coming – a “Black Swan” by Nassim Taleb’s definition. What? Another “Black Swan”? Many would say that is crazy to think that such an event could happen. Just read the previous four potential shocks and you may realize that it is not as crazy as it seems. If we take the concept of entanglement, fingers of instability and susceptibility to shock events that are low probability, high impact and coalesce them into a definition or perspective of risk we see that it is all too likely that we are looking at a transparent vulnerability. Nothing is failsafe. Nothing is assured. We can only seek to build redundant and resilient frameworks that allow us to buffer risk realization.

Conclusion: Uncertainty

Uncertainty is that factor that all our decision-making tries to guard against. We like to be in control and to believe that yesterday will predict tomorrow. We know that it is not possible to eliminate risk and uncertainty, but we do our very best through research of past history and looking for patterns that allow us to effectively predict possible future eventualities. Then, we develop procedures and plans to address these eventualities and increase our competence to handle them.

So, when dealing with uncertainty, we typically ignore it in one of two ways. One is that we may recognize the existence, depth and complexity of the problem but not take steps to confront it. An example of this is Kodak; when confronted with digital technology, refused to adapt its business model with the changing times and lost its dominance in the printing market. Another is to try to will the uncertainty into non-existence. A recent example of this was the mishandling of a cruise ship the size of a small city that became a floating “petri dish” that fostered the incubation and transfer of COVID-19. As long as the ship was not docked, the case count would not add to the national total.

There is a general lack of knowledge when it comes to rare events with serious consequences. This is due to the rarity of the occurrence of such events. In his book, Taleb states that “the effect of a single observation, event or element plays a disproportionate role in decision-making creating estimation errors when projecting the severity of the consequences of the event. The depth of consequence and the breadth of consequence are underestimated resulting in surprise at the impact of the event.”

To quote again from Taleb, “The problem, simply stated (which I have had to repeat continuously) is about the degradation of knowledge when it comes to rare events (“tail events”), with serious consequences in some domains I call “Extremistan” (where these events play a large role, manifested by the disproportionate role of one single observation, event, or element, in the aggregate properties). I hold that this is a severe and consequential statistical and epistemological problem as we cannot assess the degree of knowledge that allows us to gauge the severity of the estimation errors. Alas, nobody has examined this problem in the history of thought, let alone try to start classifying decision-making and robustness under various types of ignorance and the setting of boundaries of statistical and empirical knowledge. Furthermore, to be more aggressive, while limits like those attributed to Gödel bear massive philosophical consequences, but we can’t do much about them, I believe that the limits to empirical and statistical knowledge I have shown have both practical (if not vital) importance and we can do a lot with them in terms of solutions, with the “fourth quadrant approach”, by ranking decisions based on the severity of the potential estimation error of the pair probability times consequence (Taleb, 2009; Makridakis and Taleb, 2009; Blyth, 2010, this issue).”

I leave you with an excerpt from an article on Ulysses Grant that reflects decision making in times of uncertainty.

“Once, a colonel approached Grant with a requisition order authorizing large expenditures. Briefly reviewing the report, the general gave his approval, catching the colonel by surprise. Might the general want to ponder the matter a little longer? Was he sure he was right? Grant looked up. ‘No, I am not,’ he responded; ‘but in war anything is better than indecision. We must decide. If I am wrong, we shall soon find it out and can do the other thing. But not to decide wastes both time and money, and may ruin everything.’”

Geary Sikich – Entrepreneur, consultant, author and business lecturer

Contact Information: E-mail: G.Sikich@att.net or gsikich@logicalmanagement.com. Telephone: 1- 219-513-6244.

Contact Information: E-mail: G.Sikich@att.net or gsikich@logicalmanagement.com. Telephone: 1- 219-513-6244.

Geary Sikich is a seasoned risk management professional who advises private and public sector executives to develop risk buffering strategies to protect their asset base. With a M.Ed. in Counseling and Guidance, Geary’s focus is human capital: what people think, who they are, what they need and how they communicate. With over 30 years in management consulting as a trusted advisor, crisis manager, senior executive and educator, Geary brings unprecedented value to clients worldwide. Geary has written 4 books (available on the Internet) over 450 published articles and has developed over 4,500 contingency plans for clients worldwide. Geary has conducted over 475 workshops, seminars and presentations worldwide.

Geary is well-versed in contingency planning, risk management, human resource development, “war gaming,” as well as competitive intelligence, issues analysis, global strategy and identification of transparent vulnerabilities. Geary began his career as an officer in the U.S. Army after completing his BS in Criminology. As a thought leader, Geary leverages his skills in client attraction and the tools of LinkedIn, social media and publishing to help executives in decision analysis, strategy development and risk buffering. A well-known author, his books and articles are readily available on Amazon, Barnes & Noble and the Internet.

References

Apgar, David, “Risk Intelligence – Learning to Manage What We Don’t Know”, Harvard Business School Press, 2006.

Chernow, Ron, “Grant” Penguin Press; 1st Edition October 10, 2017, ISBN-10: 9781594204876, ISBN-13: 978-1594204876, ASIN: 159420487X

Davis, Stanley M., Christopher Meyer, “Blur: The Speed of Change in the Connected Economy”, (1998).

Forstchen, William R. Ph.D.; “One Second After”, Forge Books; 1st edition (March 17, 2009), ISBN-10: 0765317583, ISBN-13: 978-0765317582

Kahneman, Daniel, Rosenfield Andrew M., Gandhi, Linnea, Blaser Tom, Harvard Business Review October 2016 Issue; “Noise: How to Overcome the High, Hidden Cost of Inconsistent Decision Making”

Kami, Michael J., “Trigger Points: how to make decisions three times faster,” 1988, McGraw-Hill, ISBN 0-07-033219-3

Kovach, Bill and Rosenstiel, Tom “Blur: How to Know What’s True in the Age of Information Overload” 2010, Bloomsbury USA

Levene, Lord, “Changing Risk Environment for Global Business.” Union League Club of Chicago, April 8, 2003.

Musser, George, “Spooky Action at a Distance”, Scientific American/Farrar, Straus and Giroux, Copyright 2015 by George Musser, page(s): 168-170

Orlov, Dimitry, “Reinventing Collapse” New Society Publishers; First Printing edition (June 1, 2008), ISBN-10: 0865716064, ISBN-13: 978-0865716063

Sikich, Geary W., “The Financial Side of Crisis”, 5th Annual Seminar on Crisis Management and Risk Communication, American Petroleum Institute, 1994

Sikich, Geary W., “Managing Crisis at the Speed of Light”, Disaster Recovery Journal Conference, 1999

Sikich, Geary W., “What is there to know about a crisis”, John Liner Review, Volume 14, No. 4, 2001

Sikich, Geary W., “The World We Live in: Are You Prepared for Disaster”, Crisis Communication Series, Placeware and ConferZone web-based conference series Part I, January 24, 2002

Sikich, Geary W., “September 11 Aftermath: Ten Things Your Organization Can Do Now”, John Liner Review, Winter 2002, Volume 15, Number 4

Sikich, Geary W., “Graceful Degradation and Agile Restoration Synopsis”, Disaster Resource Guide, 2002

Sikich, Geary W., “Aftermath September 11th, Can Your Organization Afford to Wait”, New York State Bar Association, Federal and Commercial Litigation, Spring Conference, May 2002

Sikich, Geary W., “Integrated Business Continuity: Maintaining Resilience in Times of Uncertainty,” PennWell Publishing, 2003

Sikich, Geary W., “It Can’t Happen Here: All Hazards Crisis Management Planning”, PennWell Publishing 1993.

Sikich Geary W., “The Emergency Management Planning Handbook”, McGraw Hill, 1995.

Sikich Geary W., “Black Swans or just Wishful Thinking and Misinterpretation?” 2010.

Sikich, Geary W., “Risk the Nature of Uncertainty”, 2016

Sikich Geary W., “Can You Calculate the Probability of Uncertainty?” 2016.

Sikich Geary W., Stagl, John M., “The Economic Consequences of a Pandemic”, Discover Financial Services Business Continuity Summit, 2005.

Tainter, Joseph, “The Collapse of Complex Societies,” Cambridge University Press (March 30, 1990), ISBN-10: 052138673X, ISBN-13: 978-0521386739

Taleb, Nicholas Nasim, “The Black Swan: The Impact of the Highly Improbable”, 2007, Random House – ISBN 978-1-4000-6351-2

Taleb, Nicholas Nasim, “The Black Swan: The Impact of the Highly Improbable”, Second Edition 2010, Random House – ISBN 978-0-8129-7381-5

Taleb, Nicholas Nasim, “Fooled by Randomness: The Hidden Role of Chance in Life and in the Markets”, 2005, Updated edition (October 14, 2008) Random House – ISBN-13: 978-1400067930

Taleb, N.N., “Common Errors in Interpreting the Ideas of The Black Swan and Associated Papers”; NYU Poly Institute October 18, 2009

University of Foreign Military and Cultural Studies, http://usacac.army.mil/organizations/ufmcs-red-teaming

Vail, Jeff, “The Logic of Collapse”, www.karavans.com/collapse2.html, 2006

Vembunarayanan, Jana. “Risk vs Uncertainty”, 2013 (https://janav.wordpress.com/ https://janav.wordpress.com/author/jvembuna/

Venezuelan natural gas rig sinks; http://news.bbc.co.uk/go/pr/fr/-/2/hi/americas/8679981.stm, Published: 2010/05/13 14:38:59 GMT © BBC MMX

Weick, KE 1993, “The Collapse of Sensemaking in Organizations: The Mann Gulch Disaster”, in Administrative Science Quarterly, Vol. 38, No. 4 (Dec., 1993), pp. 628-652

Weick, KE 1995, “Sense-making in organizations”, Sage Publications

Weick, KE 2001, “Making Sense of the Organization”, Blackwell Publishers

Weick, KE, Sutcliffe, KM, and Obstfeld, D. 2005, “Organizing and the Process of Sense-making” Organizational Science, Vol. 16, No. 4, pp. 409–41

https://en.wikipedia.org/wiki/Debt_relief

https://www.entrepreneur.com/article/331198